Chelsea_Sun ・ 8 hours ago

Chelsea_Sun ・ 8 hours agoNextFin News -- Within just two days, two leading Chinese embodied intelligence companies released their prospectuses one after another. Behind the IPO buzz, the industry’s most unvarnished reality is being laid bare more clearly than ever.

On May 19, the Shenzhen Stock Exchange accepted the ChiNext IPO application of Leju Robot (Shenzhen) Co., Ltd. It also became the first company to apply for listing under ChiNext’s fourth set of standards.

Founded in 2016, Leju Robot initially entered the market through basic programming education, later launched its first small humanoid robot product, and then began moving into full-size humanoid robots in 2018.

The most eye-catching set of figures in the company’s prospectus is that in 2025 it sold 577 units of its full-size humanoid robot Kuavo series—up 17 times from 32 units in 2024.

The unit surge in sales propelled Leju Robot into the top tier of the embodied-intelligence industry that year. In 2025 sales reports by both Omdia and Counterpoint Research, Leju Robot ranked fourth globally, behind Unitree, AgiBot, and UBTECH.

But the other side of the coin is that the average selling price of the Kuavo series products fell 25.56% year on year in 2025.

Leju Robot explained in its prospectus that, to consolidate and enhance the market competitiveness of its products, the company implemented an aggressive market-oriented pricing strategy and proactively lowered the selling price of the Kuavo series.

2025 was widely seen as the first year of commercialization for embodied intelligence: explosive unit growth, revenue doubling, and global market share surging into the top ranks, yet gross margin declining for two straight years and losses widening instead.

The biggest question left for investors now is: Is this an unavoidable cost on the eve of scaling up, or a gamble of trading price for volume?

Selling Robots at 25% Off

ChiNext’s fourth set of standards requires that a listed company have an expected market capitalization of no less than RMB 3 billion, operating revenue of no less than RMB 200 million in the most recent year, and a compound annual revenue growth rate of no less than 30% over the past three years.

Leju Robot fit those requirements perfectly.

According to the prospectus, Leju Robot’ post-money valuation in its most recent financing round was RMB 4.327 billion. Taking into account the valuation levels of comparable listed companies in the same industry, the company expected its market capitalization to be no less than RMB 3 billion. In addition, its 2025 operating revenue was RMB 258 million, and its three-year compound revenue growth rate reached 118.68%.

Leju Robot plans to issue no more than 20 million shares this time, and no less than 25% of the company’s total share capital after the offering. It aims to raise a total of RMB 2.6 billion, implying an IPO valuation of roughly RMB 10 billion—placing it in the top tier of the embodied-intelligence sector.

Humanoid-robot sales also sit in the top tier.

According to Counterpoint Research, Leju Robot’ humanoid-robot shipments accounted for about 5% of the global market in 2025, ranking fourth.

Different data firms use different methodologies. Under IDC’s methodology, Leju Robot ranked third. In both sets of data, Leju Robot’ shipment volume was extremely close to UBTECH’s, with each edging out the other depending on the metric.

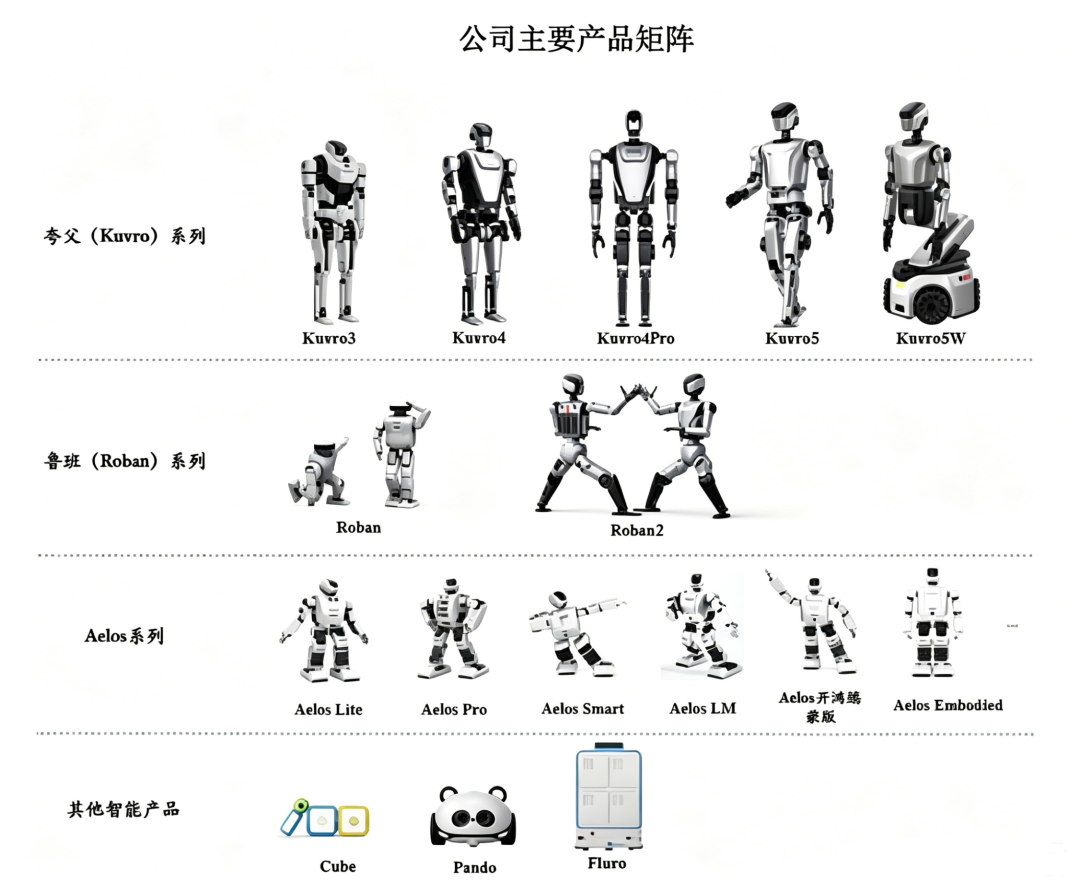

Leju Robot is a very “pure-play” humanoid-robotics company. Its products mainly fall into three categories: the Kuavo series of full-size humanoid robots, designed for broad scenarios with a particular focus on industrial applications; the Roban series of mid- to small-sized humanoid robots, aimed primarily at AI and embodied-intelligence research and education; and the Aelos small robot, geared mainly toward AI literacy and primary education.

What supported Leju Robot’ No. 4 global ranking in 2025 was the Kuavo series.

In December 2023, Leju Robot launched Kuavo3 and brought it to market. In 2024, it completed two iterations—Kuavo4 and Kuavo4 Pro. In October 2025, it released Kuavo5 and Kuavo5-W. Five product updates in three years is clearly faster than the industry’s average pace of “once a year.”

The prospectus shows that Kuavo series sales revenue reached RMB 178 million in 2025, accounting for 69.5% of that year’s operating revenue, making it the company’s main source of income.

Driven by Kuavo, the company’s overall revenue also surged. From 2023 to 2025, Leju Robot’ operating revenue was RMB 54 million, RMB 56 million, and RMB 258 million, respectively.

This growth curve closely mirrors the rise in Kuavo sales: largely steady in 2023 and 2024, followed by a sudden spike in 2025—due in no small part to the flagship product being sold at a “25% off” discount.

The prospectus shows that in 2025, Kuavo’s unit selling price fell by 25.56%. The good news was that economies of scale delivered some cost advantages: over the same period, unit cost dropped 27.35% year on year. As a result, the product’s gross margin didn’t decline and instead edged up slightly.

However, Kuavo’s surging sales reshaped the company’s revenue mix. Revenue contributions from the Roban and Aelos series—both with higher gross margins—declined, pulling the company’s overall gross margin down from 50.45% in 2023 to 44.3% in 2024, and further to 40.78% in 2025.

In step with the continued slide in gross margin was a widening net loss. During the reporting period, Leju Robot’ net losses attributable to shareholders of the parent company were RMB 41.12 million, RMB 59.23 million, and RMB 69.78 million, respectively. After excluding non-recurring gains and losses, the net loss in 2025 expanded further to RMB 77.64 million.

In addition, the company’s net cash flow from operating activities was negative for three consecutive years.

In the prospectus, Leju Robot stated that although the company had remained loss-making over the past three years—and the losses had continued to grow—this was broadly consistent with the industry’s development characteristics: heavy upfront investment is needed to build technological and product barriers.

Based on its actual operating conditions, Leju Robot also provided its own timeline for turning profitable——2028.

Leju Robot's Management

The founding team of Leju Robot largely came from Harbin Institute of Technology.

Founder and chairman Leng Xiaokun holds a PhD in Computer Application Technology from Harbin Institute of Technology. In 2016, he co-founded Leju Robot with a group of classmates from HIT.

In the same year the company was established, Leju Robot launched its first small humanoid robot, Aelos, establishing basic programming education as its initial market entry point. In 2017, the Aelos education edition began mass deliveries and started generating revenue.

Over the following years, Leju Robot largely focused on the education market. The prospectus shows that in 2025, Leju’s sales of small and mid-sized humanoid robots for the education market remained strong: 91 units of Roban were sold, and 3,988 units of Aelos were sold. Together, the two products generated revenue of RMB 39.4481 million, up 47.35% year on year.

While its education-robot products provided Leju Robot with cash flow, they also helped the company build out a nationwide sales network and after-sales service system. The prospectus shows that during its push into the education market, Leju developed a hybrid “direct sales + non-direct sales” model, establishing channel resources with broad coverage and fast response.

When Kuavo was launched in 2023, this channel system could be reused directly.

In addition, the main buyers in the education market are typically universities, research institutes, and education authorities. These customers’ procurement processes, technical integration methods, and after-sales requirements share similarities with the data-collection centers and industrial clients that Kuavo later targeted, allowing the company to accumulate B2B and B2G customer-service experience.

However, the education market has a relatively low ceiling. As a result, in 2023 Leju Robot shifted the company’s strategic focus from education to general-purpose, full-size humanoid robots. That year also marked the point when the broader embodied-intelligence industry began to heat up.

As of the end of the reporting period covered by the prospectus, Leju Robot’ full-size humanoid robot products were mainly applied in three scenarios: scientific research and education, commercial services, and data collection, while industrial manufacturing was still in its early stages.

Among these, data collection was Kuavo’s primary application scenario. In 2025, revenue from this scenario accounted for 45% of total revenue for the product line; scientific research and education and commercial services accounted for 32.5% and 18.7%, respectively, while industrial manufacturing contributed only 3.88%.

The scarcity of real-world interaction data has been a long-standing challenge for the industry, which is why data collection is foundational for humanoid robots to achieve generalization.

Data sources for model training can be broadly divided into three categories: internet data, simulation data, and real-world data. Because humanoid robots have physical embodiments, internet and simulation data alone are insufficient to support learning the wide range of physical laws encountered in the real world.

Real-world data is the highest quality, but it relies heavily on collecting data from the robots themselves. As a result, at this stage, many humanoid-robot platform manufacturers have chosen data collection as a viable path to commercialization.

Some build their own data-collection centers, such as Zhiyuan, while others sell robots to data-collection centers—Leju Robot is one of them.

According to disclosures in the prospectus, Leju Robot is currently one of the companies with the largest number and scale of commercial orders for data-collection and training scenarios.

Industrial scenarios, meanwhile, represent another type of long-cycle customer. In 2025, Leju deployed Kuavo 4 Pro at a FAW plant to conduct POC (proof-of-concept) validation for scenarios such as tote handling and picking. For industrial customers, POC is a standard step before large-scale procurement, meaning that Leju’s revenue contribution from automotive manufacturing was still quite limited and remained in the reliability-validation stage.

Beyond that, Leju Robot’ roster of shareholders and partners also includes major companies such as Tencent and Huawei.

In December 2023, Leju Robot released the Kuavo 3 powered by HarmonyOS, becoming one of the first humanoid-robot makers to integrate with HarmonyOS. In 2024, it was added to the collaboration roster of Huawei’s Global Embodied Intelligence Industry Innovation Center. In June 2025, it joined forces with Huawei and China Mobile to launch the world’s first 5G-A humanoid robot.

Meanwhile, Tencent --through its wholly owned subsidiary—holds a 7.32% stake in Leju Robot, and the two sides have not yet begun business cooperation.

Cards to Play?

Riding the surge in sales of the Kuavo series, Leju Robot has pushed its way into the top tier of embodied intelligence players. The questions it must tackle next are whether its profit model can truly work—and how much value its planned IPO fundraising total of RMB 2.6 billion can ultimately deliver.

Among robot “body” companies that have already listed or have disclosed prospectuses, DEEP Robotics focuses on quadruped robots and is not highly comparable to Leju Robot. The remaining three—Unitree, Dobot, and UBTECH—overlap with Leju Robot to varying degrees and are reasonably comparable.

First, looking at the financials, on a 2025 basis: Unitree recorded revenue of RMB 1.708 billion and was already profitable; UBTECH posted revenue of about RMB 2.0 billion, with a loss of RMB 790 million; Dobot recorded revenue of RMB 490 million, with a loss of RMB 80 million.

Leju Robot has the smallest revenue scale among the four—only about 15% of Unitree’s and about 13% of UBTECH’s.

Taking revenue scale and loss size together, Leju Robot’ losses fall between UBTECH’s and Dobot’s, and its gross margin is not materially different from the average gross margin of its peers. In an embodied intelligence industry where most companies are still loss-making, Leju Robot’ financial condition is not particularly weak.

Now, let’s look at the path to profitability.

In Leju Robot’ procurement list, joint modules and controllers account for the largest share of costs, making up 19.4% and 13.67% of total procurement spending, respectively. Dexterous hands also account for 6.71%.

In the prospectus risk disclosures, Leju Robot also noted that in 2025, its purchases from Wuxi Quanzhibo accounted for 17.20% of its total annual procurement amount. Among these, purchases of joint modules from that supplier accounted for 82.82% of the company’s procurement amount for that product category—indicating a relatively high concentration in sourcing joint modules from a single supplier.

Heavy reliance on a single external supplier for core components not only drives up costs, but also increases risk.

Compared with Unitree, which has already turned a profit, Unitree has a higher share of core components that are developed and manufactured in-house. Its joint modules and dexterous hands are already mature products—not only does it not need to source them externally, they also generate revenue for the company.

This shows that Leju Robot still has significant room to increase the in-house manufacturing rate of its core components, which is also one of the most effective ways to improve the company’s gross margin.

As for how it plans to use the proceeds raised from its public offering, unlike Unitree and Deep Robotics, which put the bulk of their funds into research on the robot “brain,” Leju Robot has chosen to invest most of the money it raised in three areas: capacity expansion, centralized/standardized operations, and data collection.

Specifically, 36.14% of the funds will be used for the Humanoid Robot Embodied Intelligence R&D Center project. Through a centralized model, the company will systematically enrich its technology reserves, focusing on breakthroughs in key links such as toolchain development, core algorithm upgrades, and body/structural design; 23.7% will go toward the High-Quality Large-Scale Dataset Development project; and 8.22% will be used for the Humanoid Robot Industrialization Base project, mainly to purchase production and testing equipment, build standardized workshops, and increase manufacturing capacity.

On the one hand, this is because Leju Robot set out from the start on a full-stack “brain–cerebellum–on-device” path, and already has a certain amount of core technical accumulation in motion control and intelligent decision-making—so for now it doesn’t need to make up extra ground at the “brain” layer.

On the other hand, its choice of fund allocation suggests that, compared with pursuing a smarter brain, Leju Robot currently places greater emphasis on real-world industrial applications of its core robot products.

After all, for today’s embodied-intelligence industry, being able to truly “go into the factory and tighten screws” is a better story than merely proving out a profitable business model.

LIKE 0

LIKE 0